Moderate Construction Growth with Increase in New Orders

MARCH DATA HIGHLIGHTED another rise in UK construction output, helped by a moderate increase in new orders.

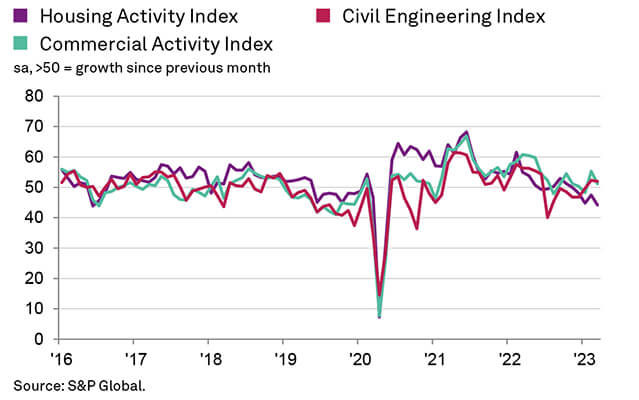

The civil engineering category saw the fastest rise in business activity, while house building was the weakest-performing area. Lower volumes of residential building work have now been recorded for four months in a row.

Supply conditions improved in March, reflecting greater availability of construction products and materials, alongside fewer logistics bottlenecks. The overall improvement in vendor performance was the strongest since November 2009.

At 50.7 in March, the headline seasonally adjusted S&P Global / CIPS UK Construction Purchasing Managers’ Index (PMI) – which measures month-on-month changes in total industry activity – was down from 54.6 in February but above the 50.0 no-change threshold for the second month running.

The latest reading signalled a marginal overall increase in total construction output. Civil engineering activity (index at 52.0) was the fastest growing area of construction output in March. Survey respondents again cited a boost from work on HS2 infrastructure projects and robust demand for other transport-related construction activity.

Increase in Commercial Building

The latest survey also signalled an increase in commercial building work (index at 51.1), although the rate of expansion eased from February’s nine-month high.

Meanwhile, housing activity (index at 44.2) decreased at a sharp and accelerated pace in March. The rate of decline was the fastest since May 2020, with survey respondents often citing fewer tender opportunities due to rising borrowing costs and a subsequent slowdown in new house building projects.

Despite subdued housing market conditions, latest data signalled a further increase in total new work received by construction companies. The latest rise was the second fastest since July 2022.

Greater workloads led to a solid upturn in staff recruitment, with the rate of job creation accelerating to its fastest since last October. That said, some construction firms noted that elevated wage pressures and shortages of available candidates had acted as a constraint on hiring.

Purchasing activity was broadly unchanged in March. Some construction companies suggested that improved supply conditions had encouraged them to run down inventories.

March data signalled the fastest improvement in suppliers’ delivery times for more than 13 years. Survey respondents widely noted that an improved balance between demand and supply had helped to boost the availability of construction products and materials.

Input prices continued to rise sharply in March, with construction companies often noting that suppliers had attributed this to elevated energy costs and rising staff wages. That said, the latest round of cost inflation was the second-slowest since November 2020.

Finally, around 46% of the survey panel predict an increase in business activity during the year ahead, while only 11% foresee a reduction. The resulting index reading signalled the strongest degree of positive sentiment since February 2022. Optimism has rebounded strongly from the two-and-a-half year low seen in December, largely reflecting signs of a turnaround in client spending and a more favourable outlook for the wider UK economy.

COMMENT

Tim Moore, Economics Director at S&P Global Market Intelligence

Tim Moore, Economics Director at S&P Global Market Intelligence, which compiles the survey said: “UK construction companies experienced a sustained rebound in output levels during March as work on civil engineering and commercial projects picked up for the second month running. Improved tender opportunities were also reflected in an upturn in new orders since February and the strongest rate of job creation for five months.

“A sharp and accelerated decline in house building was the main area of concern in March. Cutbacks to new residential projects in the wake of subdued demand and rising interest rates contributed to the sharpest fall in housing activity across the construction sector for almost three years.

“Despite worries about the near-term outlook for housing activity, expectations for total construction output during the year ahead were relatively upbeat in March. Growth projections were boosted by the fastest improvement in suppliers’ delivery times for more than a decade. Survey respondents often cited improved availability of construction inputs and subsequent hopes that purchasing price inflation would moderate in the months ahead.”

Dr John Glen, Chief Economist at the Chartered Institute of Procurement & Supply

Dr John Glen, Chief Economist at the Chartered Institute of Procurement & Supply, said: “A small uplift in construction activity in March shows the sector is heading in the right direction and at a stabilising pace, and with a few uplifting surprises along the way.

“Delivery times from suppliers improved at the fastest rate since November 2009 as stocks were unravelled and fewer orders from supply chain managers meant goods got through more quickly. Builders were also riding high with the highest levels of optimism since February 2022 and there was an uplift in hiring levels to maintain momentum.

“Strong inflationary pressures remained an obstacle to wider expansion at building companies however along with concerns over consumer affordability rates. With residential building still struggling and falling at the fastest rate since May 2020, it was the bigger projects like HS2 managed by the civil engineering sector that added fuel to the engine of construction growth this month.”

INDUSTRY COMMENT

Sector Must Promote Itself

Joe Sullivan, partner at MHA

Joe Sullivan, partner at MHA, comments: “The Spring Budget may not have shocked the sector but did little to inspire or help the housing or commercial markets over the long term. Contractors still engage with fixed price or even loss-making contracts, prioritising short-term cash inflow and team retention over medium-term profitability and working capital funding. Management teams need to be open minded about renegotiating contract terms and retain a forensic understanding of which overhead elements can be reduced swiftly to avoid future financial distress.

“Similarly, shortage of labour is now the single biggest headache for the sector. Vacancies in the sector have risen at a faster rate than across the economy as a whole, illustrating the need for the government to provide help quickly. Adding construction roles to the Shortage Occupation List is a welcome move, but this measure is only interim and won’t be implemented until the Summer, bringing into question its effectiveness. The policy may also not deliver similar rates across the country, as traditionally the South East and London have benefitted most from migrant labour.

“It is clear stakeholders are moving towards improving recruitment and retention, this is too little and too slow. The sector must promote itself as an appealing industry for school leavers and graduates to have a sustained future.”

>> Read more construction data in the news

The post Moderate Construction Growth with Increase in New Orders appeared first on Roofing Today.